ŌĆ£Budget 2026 is a declaration that Trinidad and Tobago is back on course… When UNC wins, everybody wins!ŌĆØ

Minister of Finance, Davendranath Tancoo.

Photo: Office of the Parliament 2025.

The desk thumping and back slapping in response to the Budget delivery reminded me of the declaration by US President George Bush in 2003.

After six weeks of fighting in Iraq, he declared mission accomplished. The war went on for another eight years.

It is evident that Dr Indera Sagewan, an economist recently appointed to the Central BankŌĆÖs board, had concerns. In addressing the Trinidad and Tobago ManufacturersŌĆÖ Association (TTMA) post-budget forum, she characterised the Budget as ŌĆ£the first major policy statementŌĆØ.

Copyright: Office of the Parliament 2025.

She cautioned: ŌĆ£We are in such a difficult place. It is now more than ever that we need a sense of confidence, a sense of hope, a sense that those who are in the driverŌĆÖs seat have a destination in mind and they are taking us with them on that journey to a destination that is going to be a bright and prosperous one.ŌĆØ

This single statement encapsulates two pertinent facts: confidence is a requirement for success, and achieving our national goals, however we define them, will take time.

We do not include the issue of consumer and business confidence in our Budget discussions. We do not often think about inducing confidence by the multilateral financial institutions. Instead, we focus on the measures announced.

Dr Nigel Clarke, the deputy managing director of the IMF and former finance minister of Jamaica (2018 ŌĆō 2023), indicates that there is no quick fix to redirecting a nationŌĆÖs course. He warned: ŌĆ£Great danger exists if we believe that the growth challenge can be addressed with quick fixes.ŌĆØ

Sagewan also understood the political risks: ŌĆ£You have now set the stageŌĆ” If you fail to deliver or be well on the way to deliveryŌĆ” next year wonŌĆÖt be so easy.ŌĆØ

This analysis of our Budget uses this framework of the perspectives of consumers and businesses.

Consumer spending is the key to any market economy. Because consumer spending accounts for between 50% to 75% of the gross domestic product, it is the most vital component of any economy.

To measure total consumption, we can use consumer sentiment as our marker. Measuring the consumption of durable goodsŌĆösuch as appliances, furniture, electronics, and cars ŌĆöalso serves as an indicator of consumer spending.

The real test is ŌĆ£do consumers believe that their future will be better?ŌĆØ

For the average consumer, the implications are not always immediately evident. Budget presentations often serve political purposes. An analysis of it is needed to identify potential risks and challenges for our consumers.

Even when politicians and technocrats discuss the Budget, the wider public may still struggle to interpret the discussions. The former is often used as an opportunity to deliver a barrage of political picong.

The net effect on consumers will be revealed shortly. We will see the knock-on effect at the retail level. The consumer will understand what is left in their pockets to face their demands.

Businesses, however, are more attuned to every aspect of the Budget.

Corporate spending closely mirrors the role the stock market has played in most recoveries, and dramatic changesŌĆöup or downŌĆöcan be seen as a leading indicator of what the business community is thinking.

We have witnessed the stock price changes for FCB and will now observe Angostura as another market indicator of business confidence. We can also consider the demand for services like advertising and information technology as a gauge.

Business confidence comes not from the challenges themselves, but from how much better the sector and the government are prepared to face them.

Have the government leaders who engaged with the business leaders persuaded them that they can handle the future challenges?

The elephant in the room is capital flight. For example, in January 2003, the high-net-worth clients of several money market funds asked for their money to be moved outside of Jamaica. They had no interest in any product with sovereign risk.

This action was their response to the S&PŌĆÖs downgrade in December 2002. That downgrade was triggered by reckless political action.

The S&PŌĆÖs decision led to the collapse of the Jamaican dollar from $50 to $70. This decline led to additional stress on the domestic financial sector.

Do we have any sense of what is happening on the local scene?

Senator Vishnu Dhanpaul asked a pertinent question about the disappearance/ movement of US Dollars, but nobody bothered to answer him.

On the heels of the Mid-Year Review, there also appear to be borrowings/ withdrawals from the Heritage and Stabilisation Fund, but there has been no acknowledgement or explanation. Such actions reduce the economyŌĆÖs ability to respond to shocks.

Another indicator of business confidence is the rise in interest rates. If we need the local interest rates to be juiced, we should also expect trouble to be not far off.

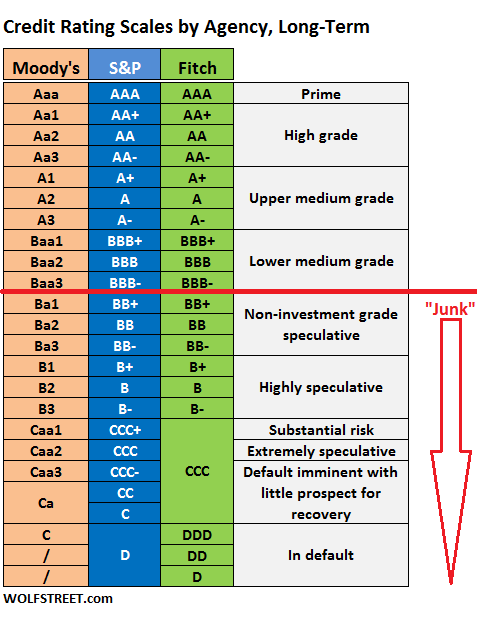

Credit ratings by institutions, such as S&P, are opinions about the future national ability to repay its debt. These institutions examine events that may impact the nationŌĆÖs relative creditworthiness. They examine the economyŌĆÖs structure/ diversification, as well as its growth and stability.

They also consider how well the government manages economic and financial policies. Critically, it evaluates the governmentŌĆÖs revenue and expenditure trends.

Fiscal discipline and manageable debt levels are key indicators of good health.

We should assess the governmentŌĆÖs performance over the last few months. Nigel Clarke of the IMF noted: ŌĆ£Our advice to policymakers on how to rebuild buffers and strengthen frameworks is straightforward: mobilise tax revenue, spend wisely, and plan ahead.ŌĆØ

Copyright: Office of the Parliament 2025.

Did the Budget follow the advice given? What does running down of the reserves mean for the future management of the national debt?

We chose to defy the IMFŌĆÖs advice about tax revenues via the Revenue Authority.

Now, we have received some sobering news. Our growth trajectory has dimmed, and inflation estimates are up. Such problems are not solved by partisan finger-pointing.

The banking sector is of particular interest to the rating agencies. The government has established a new board for FCB and has pledged to utilise its authority to appoint the majority of the Republic board.

(via Flckr.)

Will these banks, which account for the majority share of the local banking sector, continue to be stable and withstand stress?

Stress testing reveals how stable the banks will be in times of severe conditions. Credit losses during recessions or sharp interest rate hikes are simulated.

Has the government displayed an understanding of these issues? Are the new board members capable of guiding the banks in these exercises so that they can take corrective actions?

Photo: Nicholas Bhajan/ Wired868.

Will they be able to engage the credit rating agencies in discussing the proposed actions?

Is the interest in the banks driven by a need to do a debt swap, where lower-cost options replace the higher-cost debt?

The proposed levy on the banksŌĆÖ assets will impact their lending practices and portfolios. This action is not only about passing on the price to the retail or business customer.

Can the new board assist in the requisite scenario building? What will happen to the mortgage market? What will depositors do? What will shareholders do?

The Budget spoke to the issue of accountability. But in Jamaica, there were laws passed to ensure that the accountability was transparent.

The Banking community was also a critical member of the monitoring team. Peter Phillips, the Jamaica finance minister, said: ŌĆ£You had all these bankers in conjunction with the IMF monitoring the program and reporting out to the people every quarter what was going on, what was the progress. And if there was slippage, whereŌĆÖs the slippage.ŌĆØ

How would this scenario play out in our environment if the government were to seize control of the major banks?

Sagewan did not articulate the ŌĆ£difficult placeŌĆØ, but Mia Mottley did.

ŌĆ£Our world is in crisis. I will not sugarcoat it. These are among the most challenging of times for our region since the majority of our members gained their independence.

ŌĆ£Indeed, it is the most difficult period our world has faced since the end of World War II, 80 years ago.ŌĆØ

In an earlier column, we warned that we were sleepwalking into problems.

The government has openly hitched its wagon to the Trump administration. The Caribbean, and most certainly we, now face the risk of armed conflict. The Budget did not address this risk. The desire for the Dragon Field earnings was dominant, and we did not discuss our mitigation plan.

There has been considerable discussion about the price of oil and gas used in constructing the revenue estimates. There are two matters that we ought to bear in mind.

Firstly, there is an expected increase in supply. ŌĆ£We expect global oil inventories to rise through 2026, putting significant downward pressure on oil prices in the coming months. We forecast that the Brent crude oil price will fall to an average of $62 per barrel (b) in the fourth quarter of 2025 and $52/b in 2026.ŌĆØ

ŌĆ£Lower natural gas prices largely reflect our expectation that US natural gas production will be higher than previously forecast, leading to more natural gas in storage compared with our previous forecast.ŌĆØ

We saw a slight reference to the shift from fossil fuels in our Budget. But in the rest of the world, this is the scene.

ŌĆ£We project global electricity generation will increase by 30% to 76% in 2050 from 2022 (depending on the case) and will primarily be met by zero-carbon technologies across all cases.

ŌĆ£For all cases, we project that 81% to 95% of the new electric-generating capacity installed from 2022 to 2050 to meet new demand will be zero-carbon technologies.

ŌĆ£As a result, by 2050, the combined share of coal, natural gas, and petroleum liquids will decrease to between 27% and 38% of the installed global generating capacity across our cases.ŌĆØ

Are we preparing for the zero-carbon future? How do we reconcile that future with our desire to resurrect the refinery? What does this resurrection mean for the huge debt/bond being carried by Heritage Petroleum?

On the positive side, we have finally faced the NIS looming nightmare. In 2021, then Finance Minister Colm Imbert faced a furious attack from the then-Opposition and the Public Service Association when he raised the issue of increasing the retirement age.

It was Brian Manning who stood to refute the claims made by MP Tancoo.

Copyright: Office of the Parliament 2022.

However, we should note that the extension of the retirement age is only one recommendation to fix our demographic mess. We must acknowledge that our Senior CitizensŌĆÖ Pension is currently at 115 per cent of the minimum wage, while the NIS minimum pension is 99 per cent.

In some cases, there is no recognition of additional years of service in the pension paid.

ŌĆ£This actuarial valuation shows that the current contribution rate must be increased, and at least during a transitional period, some modifications to the benefits must be made, but it will not be enough.ŌĆØ

The inclusion of the self-employed is a ŌĆśmustŌĆÖ. The actuaries pointed to other countries such as Argentina, Brazil and Uruguay as templates of such extensions.

There is a need for a better integration of the entire local system and a change in the pension formula from the complicated earnings class system to a formula based on a percentage of earnings.

The NIS journey now starts.

There was no mention of the circular debt trap between WASA, T&TEC and the Desalination Company (DesalCoTT). T&TEC has a billion-dollar debt.

Approximately 55% of that is owed by DesalCoTT. But T&TEC owes NGC even though the gas is subsidised to the tune of about 50 per cent compared to the price at NGCŌĆÖs other markets. But WASA owes DesalCoTT.

ŌĆ£WASA has to pay Desalcott US$7 million every month for water. This is an albatross around the necks of taxpayers.ŌĆØ

DesalCoTT has a contract to 2036.

How do we solve this problem? Or is it not a problem since a key DesalCoTT executive has recently been named to the Republic board?

On the other hand, we bleed the institutional knowledge with every election.

We ignore the lessons from Jamaica. Leadership matters! Competence is needed to navigate the national ship through stormy weather.

Peter Phillips (PNP) laid the path in 2013 for Nigel Clarke (JLP) to follow in 2016. This undisturbed path led to JamaicaŌĆÖs ability to have economic stability.

Can we evaluate our leaders? Can we move away from entrenching political polarisation to help us achieve macro-economic stability?

Jamaica did not achieve substantial growth. But it had economic discipline, and it removed the polarisation that would have hindered its stability. ┬ĀCan we do that? The collective Caribbean experience powerfully demonstrates the transformative potential of macroeconomic stability.

Are we prepared to heed Nigel ClarkeŌĆÖs warning about productivity?

ŌĆ£Addressing the Caribbean growth challenge requires systematic and comprehensive policies to strategically improve the factors that contribute to growth potential.

ŌĆ£Zooming in on one of the important factors, the CaribbeanŌĆÖs productivity growth has declined to almost zero. This is at the root of the CaribbeanŌĆÖs growth challenge.ŌĆØ

Does anyone have data on the productivity of our civil service? Will we base our wage increases on a shaky foundation, relying on the delivery of the Dragon Field?

Photo: UNC.

We can ignore these issues, but at some time we will need to pay the piper.

This week, two quotes came to mind as I read the local newspapers. The first was from Benjamin Franklin, who Read more

ŌĆ£[ŌĆ”] For neighbouring countries [of war sites], output falls by 10% on average after five years while inflation rises by Read more

Mr Justice Ronnie Boodoosingh is worthy of holding the office of Chief Justice to which he was appointed on Wednesday Read more

ŌĆ£[ŌĆ”] While the government has made much of fiscal consolidation and social spending, it has left precious little fiscal or Read more

ŌĆ£[ŌĆ”] Yes, the tone of the budget is firm and unapologetic. It calls out past failures and demands accountability. Some Read more

ŌĆ£True ignorance is not the absence of knowledge, but the refusal to acquire it.ŌĆØ Karl Popper, Austrian-British philosopher. The recent Read more

Noble Philip, a retired business executive, is trying to interpret JesusŌĆÖ relationships with the poor and rich among us. A Seeker, not a Saint.

Now at the committee stage of the examination of the budget statement (all fluff aside) some startling details are surfacing. Again the unc is showing themselves as having little respect for the intelligence of citizens. The budget is revealing some serious policy shifts (not highlighted in the initial statement) that are likely to rock our economy and the social fabric of the nation. Citizens must be vigilant now more than ever.