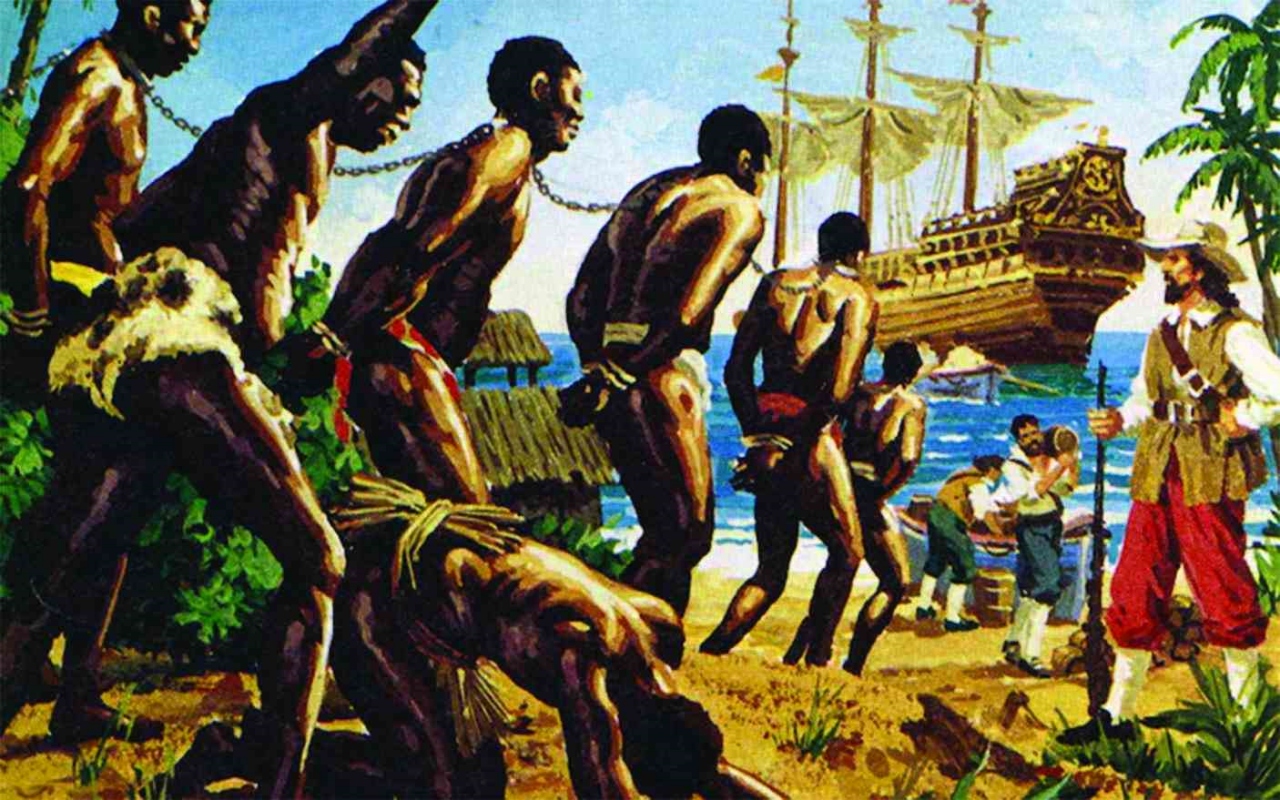

“[…] What is this claim that human people have been thrown overboard? This is a case of chattels or goods. Blacks are goods and property; it is madness to accuse these well-serving, honourable men of murder.

“They acted out of necessity and in the most appropriate manner for the cause. The late Captain [Luke] Collingwood acted in the interest of his ship to protect the safety of his crew.

(via The Standard.co.zw)

“To question the judgement of an experienced, well-travelled captain held in the highest regard is one of folly, especially when talking of slaves. The case is the same as if wood had been thrown overboard…”

Solicitor General, Justice John Lee. The Zong trial, 1783.

The Zong massacre is a classic example of how the world of finance and slavery coexisted.

The Zong was a slave ship owned by a Liverpool merchant. It was a small ship. The economics of slave trading meant that the enslaved people had to be packed closely. But even by those standards, the Zong was overloaded. It was carrying 470 persons instead of the expected 193.

The ship’s captain, Luke Collingwood, became ill during the journey. The ship overshot its destination, and the crew and the human cargo began to get sick.

Collingwood decided to “jettison” some of the cargo to save the ship and allow the ship owners to claim for the loss on their insurance. During the next week, the crew threw 130 of their cargo overboard. They were all alive.

On arriving in Jamaica, the owner filed a claim for losing the human cargo, but the insurers objected. However, they lost the case twice. According to the Solicitor General, the human cargo was no different from wood.

Marine insurance was used to insure the ships and the “West India men” carrying produce to Britain. The enslaved people were a line item of the insured cargo.

It was estimated that between 40 and 65 per cent of the marine insurance premium income of the leading London insurers came from the slave trade and products out of the Caribbean.

British willingness to advance capital and innovative ways of creating credit allowed Britain to become the dominant country in the slave trade.

The ships leaving Britain carried goods, like guns and textiles, to be used to acquire enslaved people. To feed the demand for labour, the Africans engaged in wars and raids upon each other’s villages. These raids created distrust between the tribes.

The Europeans built compounds to hold the captured people until the ships came. The ships were loaded, and the second leg of the triangle began. In the Caribbean, the newly enslaved people would be traded for produce to be taken to the cities in England.

Up to two years were needed to make the round trip, necessitating extended credit. The lives of the enslaved were the basis of the credit chain.

To understand the significance of the slave trade and the development of the credit market, we need to know that only a tiny proportion of the British-African trade in the 18th century was made up of direct trade between Britain and Africa.

In the second half of the century, when the trade reached its greatest volume, over 90% involved purchasing and shipping enslaved people to the New World.

The total investment in a medium-sized sugar plantation in Jamaica in 1774 was £13,026, excluding land value. Of this amount, the value of the enslaved people employed was £7,140, being 54.8% of the total. When the land value is included (£6,001), the proportion comes to 37.5 per cent.

The planters expected to get about fifteen years’ worth of work from them and issued a bill to the wholesalers for the purchase. Two years of work usually met the purchase price. The planter, therefore, could use the rest of the term to finance other ventures.

The wholesalers issued a bill to the slave ship captains. All these bills were taken up by London merchants who were the consignees for the sugar produced.

In some instances, new estates offered mortgages—the value of which included the enslaved people and any possible offspring, as a means of raising the needed capital. Absentee planters also created mortgages when they wanted to engage in conspicuous consumption in London or make gifts for their children.

The legacy of this way of doing business is the moral distance between those who issue the financial instruments and those whose lives are negatively impacted. Slavery was not seen by those who lived on its proceeds in England.

This situation is the same as in the USA during the 2008 financial crisis. The mortgages of poor people were packaged and sold for their future income streams.

For those issuing the bonds, the profit was risk-free. For homeowners, their adverse credit ratings and lack of financial skills made them easy prey. The mortgages were so constructed as to lock them into economic bondage.

The large firms involved were bailed out while the homeowners lost their homes. As in the case of the Zong, the court case made no difference to the lives of the survivors, and the financial products’ owners were unaffected by the losses.

Schemes such as these make individuals responsible for social problems and ignore the structural relations of austerity.

We need to examine the needs of disadvantaged communities and rectify the power imbalances in our banking and financial systems.

We must analyse the workings of our educational system. We spend large sums, but are we gaining the capacity to compete internationally?

How do we tackle the distrust between the ethnic groups, the people and the institutions? Without trust, we cannot make progress.

The lack of trust in financial institutions serves as a barrier to economic growth. The lack of trust between the ethnic groups, handed down by the planters, continues to inhibit national solidarity.

“[…] In Dr Eric Williams’ Capitalism and Slavery, he used historical analysis of a vast number of sources to put Read more

This week, two quotes came to mind as I read the local newspapers. The first was from Benjamin Franklin, who Read more

“Budget 2026 is a declaration that Trinidad and Tobago is back on course... When UNC wins, everybody wins!” Minister of Read more

As primary school children, we would have learnt a poem by John Keats. “There was a naughty boy/ And a Read more

My last topic was the cancellation of the Independence Day military parade, which was yet another issue over which there Read more

Professor Emerita Bridget Brereton, in her masterful 2010 contribution, All ah we is not one, highlights the development of competing Read more

Noble Philip, a retired business executive, is trying to interpret Jesus’ relationships with the poor and rich among us. A Seeker, not a Saint.